[ad_1]

So as to maintain capital flowing into industrial actual property offers and initiatives, traders and builders are more and more turning to different funding sources.

Picture by drical/iStockphoto.com

The pool of economic actual property lenders was already shrinking in 2022, based on information from MSCI, and up to date occasions have accelerated the tempo. “The upheaval highlights a fluid state of affairs as lenders come to grips with an atmosphere of upper rates of interest,” Jim Costello, govt director, MSCI Analysis, wrote earlier this 12 months. “Debtors within the industrial (actual property) market themselves have confronted challenges, with increased mortgage prices repressing some funding exercise.”

Larger mortgage charges are “partly a yield curve story” however “additionally one about competitors, as there have been fewer lenders originating new loans,” based on Costello.

Whereas each the industrial and multifamily sectors have been rattled by current occasions and by the specter of defaults, the industrial house is predicted to undergo extra acutely. In a June analysis transient, CenterSquare Funding Administration famous that the rental residential sector is finest positioned for personal lending alternatives, in addition to for a possible rebound.

“The needs-based demand for multifamily has resulted within the asset class experiencing resilient occupancy ranges all through historic downturns” way back to the Eighties, the agency stated in its report. Business property, in the meantime, are likelier to develop into vacant in an financial downswing, fairly than merely seeing their rents flatten or lower, based on CenterSquare.

Saul Ewing Associate Anthony Kang. Picture courtesy of Saul Ewing

“As regional banks and different institutional lenders tighten their lending necessities, multifamily property house owners undoubtedly have needed to work tougher to refinance their present debt and procure new financing for acquisitions,” stated Anthony Kang, a associate at Saul Ewing. “Some have turned to non-traditional sources, similar to non-public funds, most well-liked fairness sources, and different different lenders who usually cost increased rates of interest.”

These lenders have their very own points, nevertheless, as they navigate the identical financial tumult as everybody else. “Even among the extra established non-public debt traders are additionally slowing down as they work to handle points on their present steadiness sheet attributable to current disruptions,” stated Margaret Grossman, managing associate & president of T30 Capital, a middle-market actual property debt and fairness investor. “That stated, we’re additionally seeing new entrants into the market seeking to capitalize on rising charges.”

In the meantime, short-term loans, at all times a characteristic of economic actual property financing, have develop into more and more essential. T30 Capital is seeing its share of the motion. “We’re seeing effectively capitalized debtors look to refinance from bridge to bridge the place they could previously have exited a bridge mortgage by refinancing into a conventional time period mortgage,” stated Grossman. “We’re additionally seeing some credit score market contributors seeking to provide ‘stretch senior’ choices to cowl the hole between obtainable debt financing and fewer obtainable fairness capital.”

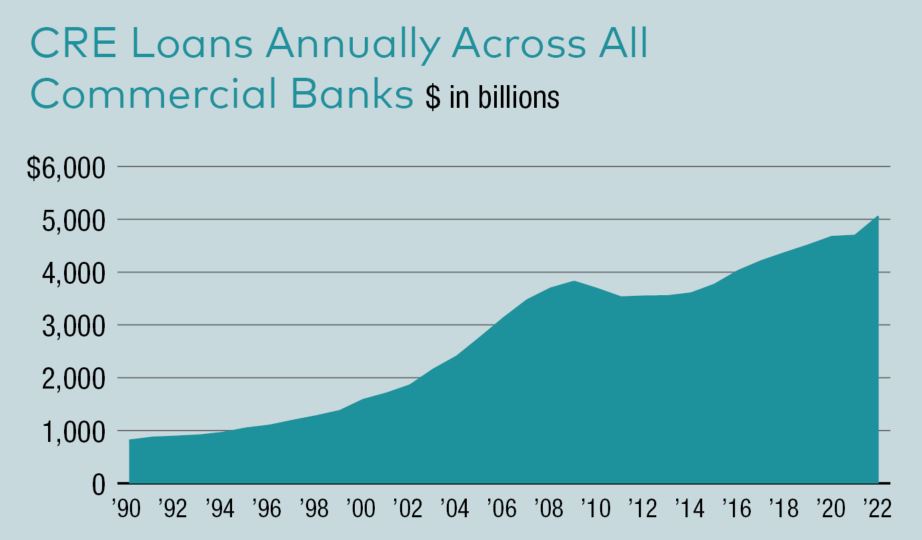

Supply: Federal Reserve Financial institution of St. Louis

A plea to Uncle Sam

Spurred on by looming maturity dates and the impacts of distant work, the Actual Property Roundtable has requested federal financial institution regulators reestablish a troubled debt restructuring program for the industrial actual property sector. The proposed program would grant monetary establishments elevated flexibility to refinance loans, mirroring related packages that have been established by federal companies in 2009, 2010, 2020 and 2022.

In an open letter to regulators, the group famous that the U.S. industrial and multifamily sectors signify a mixed $20 trillion, financed with $5.5 trillion of debt. Of that $5.5 trillion, 50.3 p.c is supplied by industrial banks. In flip, $936 billion of that $5.5 trillion matures in 2023 and 2024. Along with holding a majority of the nation’s mixed industrial and multifamily debt, industrial banks maintain nearly all of debt in every particular person sector.

The specter of mass defaults has hung over the industrial actual property house for months. Business actual property titan Brookfield Corp. rattled the sector with its default on a mortgage for a number of Washington, D.C.-area workplace properties this spring. Coming in April, on the heels of repeated financial institution collapses, the information compelled traders to confront the considered a possible wave of delinquencies. The mortgage for the Brookfield properties was transferred to a particular servicer. The next month, Brookfield defaulted on $275 million in CMBS financing for EY Plaza, a 41-story workplace tower in downtown Los Angeles. The financing was positioned in receivership. The agency additionally defaulted on $755 million in loans for the Fuel Firm Tower and the 777 Tower in Los Angeles early this 12 months.

CRE lending will get artistic

Vendor financing is at the moment one of many extra widespread different choices for debtors, stated William Kramer, a associate at Brinkley Morgan. That is partly as a result of, attributable to typically giant worth or value will increase. “Many sellers have sufficient fairness to repay any present mortgages and nonetheless have sufficient to finance a big portion of the worth for patrons,” Morgan stated.

Conventional institutional lenders are more and more cautious when underwriting loans on this high-interest charge atmosphere. “The upper charges and, thus, increased borrowing prices make it tougher for debtors to satisfy the monetary covenants similar to debt yield and debt service protection ratio,” Kramer noticed, noting that whereas rents have elevated considerably, rates of interest have greater than doubled in lots of instances in recent times.

Whereas the Fed’s current pause was assuredly simply that, some builders are wanting across the nook to a doubtlessly lower-rate atmosphere. “There may be some sentiment amongst debtors that rates of interest will come again down within the subsequent few years,” stated Kramer, “so they’re prepared to danger paying a better charge than an institutional charge to a vendor for a short-term mortgage, then refinancing.”

Associate Ronald Fieldstone. Picture courtesy of Saul Ewing

One other different gaining consideration is EB-5 financing. Administered by U.S. Citizenship and Immigration Companies, an company of the U.S. Division of Homeland Safety, the EB-5 visa program is an investment-based immigration program that permits immigrant traders to acquire everlasting residency within the U.S. in alternate for investing in a home enterprise.

“The renewed curiosity within the EB-5 program is, due largely, to Congress passing laws to revamp this system greater than a 12 months in the past,” stated Ronald Fieldstone, a associate at Saul Ewing. “The flexibleness of EB-5 financing allows builders to safe funds with a diminished reliance on senior loans and at a below-market charge, in comparison with conventional junior mezzanine financing.”

Underneath the phrases of the EB‐5 Reform and Integrity Act of 2022, this system requires a minimal funding of $1.05 million.

Weathering storms

Brinkley Morgan Associate William Kramer. Picture courtesy of Brinkley Morgan

Whereas there isn’t a assure when lending will ramp up, Kramer predicted that, as underwriting standards adjusts to a higher-interest charge atmosphere, lenders will ultimately settle for decrease charges and fewer conservative monetary covenants.

“I’m seeing from each my borrower shoppers and lender shoppers that debtors with very sturdy monetary statements are in a position to shut loans a lot faster and simpler, even the place the financials of the property is probably not as sturdy,” stated Kramer.

T30’s lending arm, Fort Amsterdam Capital, expects to see exercise proceed and presumably improve within the second half of this 12 months, based on Grossman. “The most important think about figuring out how a lot exercise will choose up will seemingly be debtors’ means to boost fairness behind their debt.”

However it isn’t solely the macroeconomic state of affairs and the particulars of economic actual property that may have an effect. Excessive climate is an element, too, since one of many largest impediments to actual property mortgage loans has been acquiring property insurance coverage.

Regardless, regardless of stormfronts each figurative and literal, Kramer speculated that capital will, in some kind, at all times be obtainable. “Lenders must generate profits, which they do by making loans. Traditionally, lenders will at all times discover a solution to make loans even in less-than-ideal lending environments.”

Learn the August 2023 concern of CPE.

[ad_2]

Source link